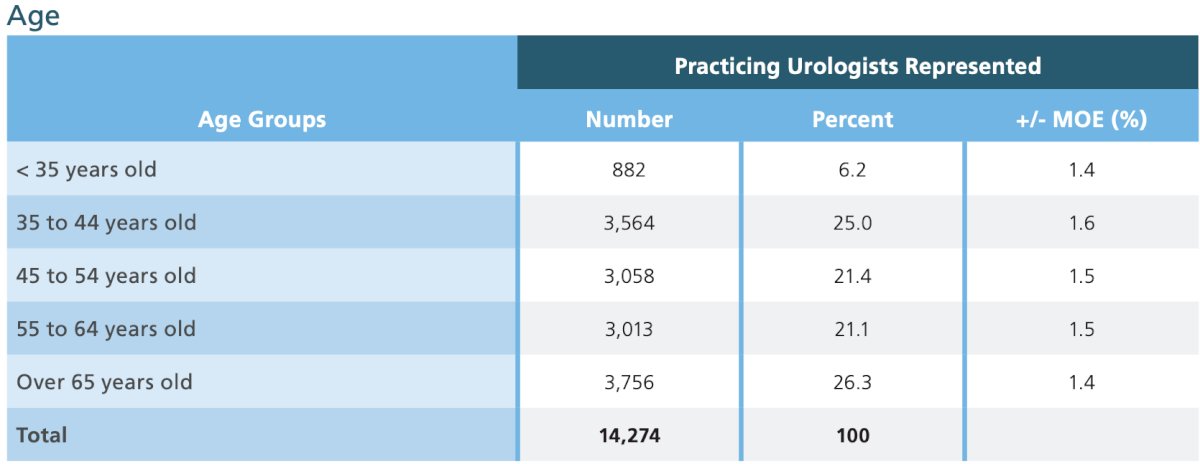

(UroToday.com) The 2026 SESAUA annual meeting featured the Gee-Dineen lecture series and a presentation by Dr. Andrew Harris discussing the state of the Urology workforce. Dr. Harris started his presentation by comparing the economics of Urology to the Rolex company: driven by supply, demand, and controlled distribution. Based on data from the 2024 AUA Annual Census, it is notable that Urology has an aging workforce. The median age of practicing urologists is 54 years, with 65 years and older being the largest age group (26.3%) of urologists:

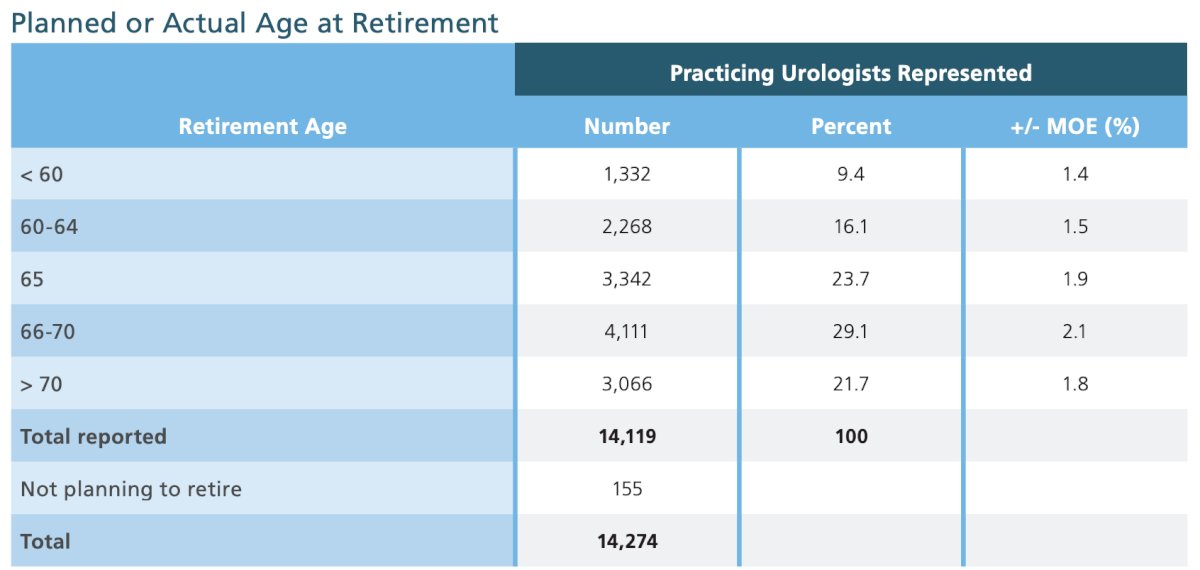

This is particularly concerning given that the mean planned or actual age at retirement among practicing urologists is 67.1 years, and only half of practicing urologists plan to work beyond age 65:

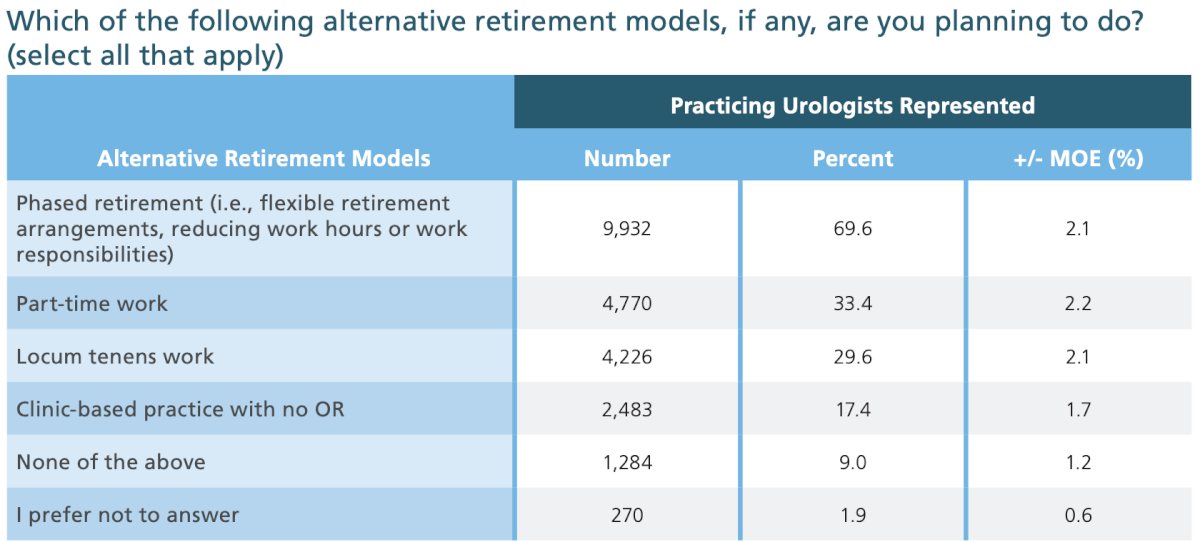

Interestingly, there may be substantial proportion of urologists that plan to use locum tenens as part of their retirement, as 70% of practicing urologists report that they are planning to do a phased retirement, 33.4% are planning to do part-time work, 29.6% are planning to do locum tenens work, and 17.4% are planning to do clinic-based work with no operative cases as alternative retirement models:

In a study by Nam et al.,1 they performed a study projecting the US Urology Workforce for 2020-2060. In a continued growth model, 2030 will have the lowest number of urologists per capita of 3.3 urologists per 100,000 persons, and recovery to baseline will occur by 2050. There are 23.8 urologists per 100,000 persons aged 65 years and older in 2020, which decreases to 15.8 urologists per 100,000 persons aged 65 years and older in 2035 and never recovers to its baseline level by 2060:

In a stagnant growth model, there will be a continued decrease of urologists per capita to 3.1 urologists per 100,000 persons by 2060. There is a continued decrease in per capita urologists at each time point, with 13.1 urologists per 100,000 persons aged 65 years and older by 2060:

What’s important to note is that with the impending urology workforce shortage, there will be an exaggerated shortage of total urologists per person aged 65 years and older in both models.

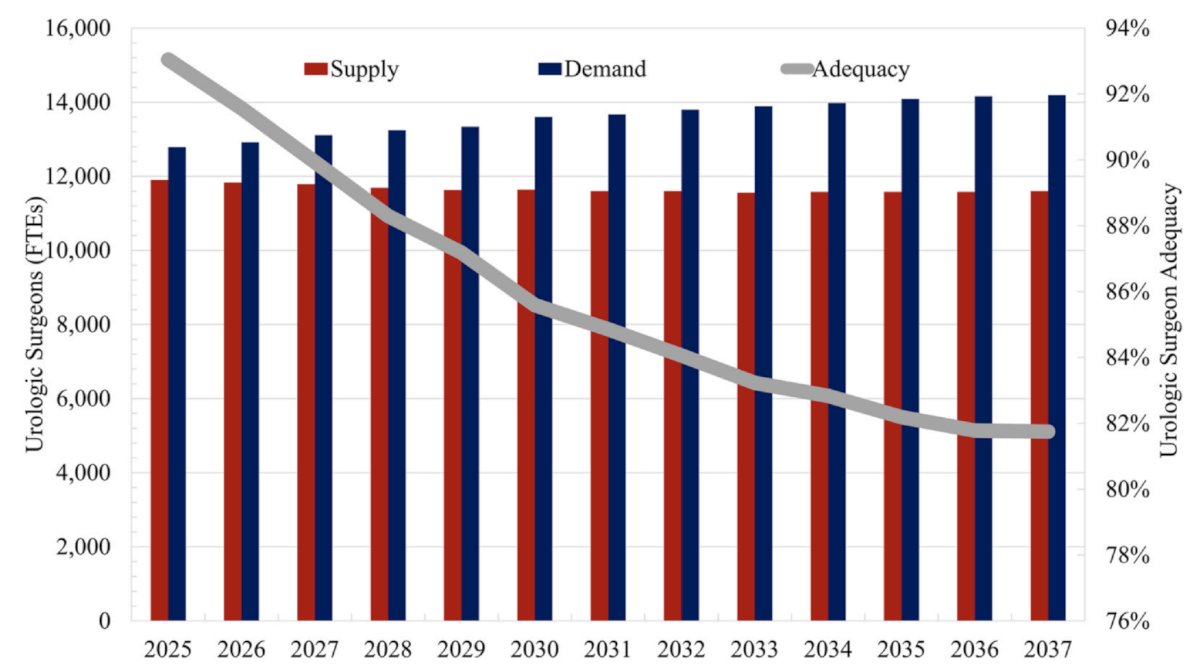

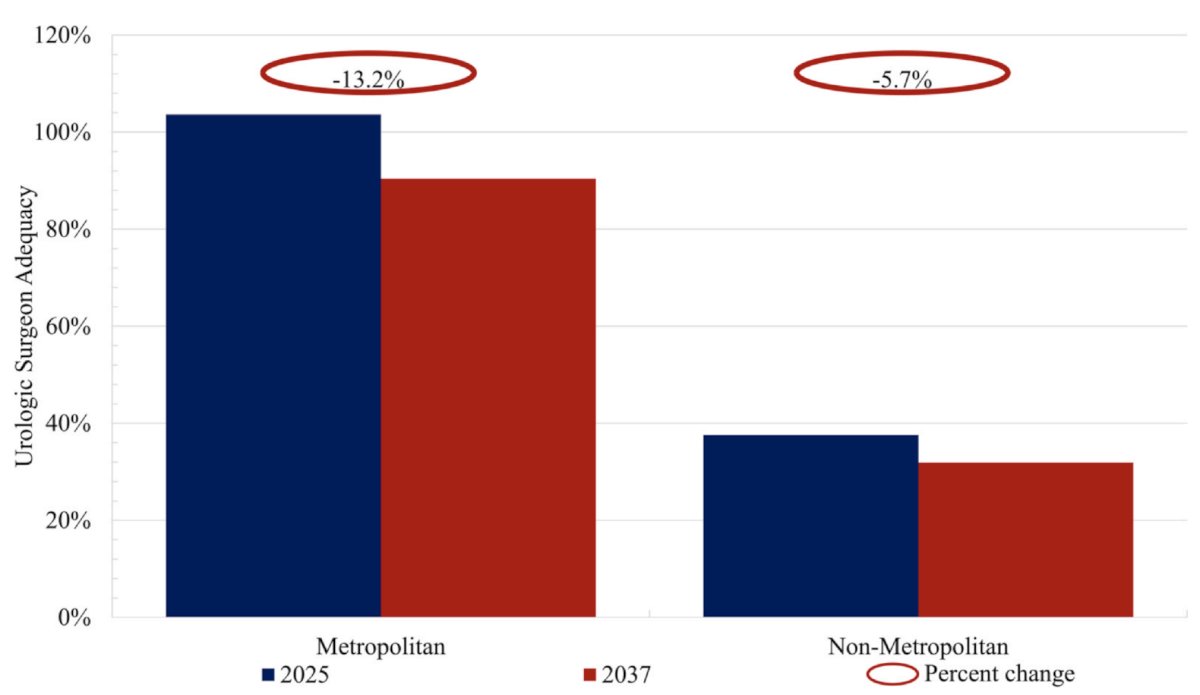

In 2025, Silvestre and colleagues2 assessed the national projections of the supply, demand, and adequacy of urologic surgeons in the United States. Using a cross-sectional study, they found that from 2025 to 2037, the supply of urologic surgeons decreased (11,900-11,600, 2.5% decrease, p < 0.001) while the demand for urologic surgeons increased (12,790-14,190, 10.9% increase, p < 0.001). As a result, urologic surgeon adequacy decreased over the study period (93.0%-81.7%, p < 0.001).

Non-metropolitan areas had lower adequacy of urologic surgeons than metropolitan areas (p < 0.001):

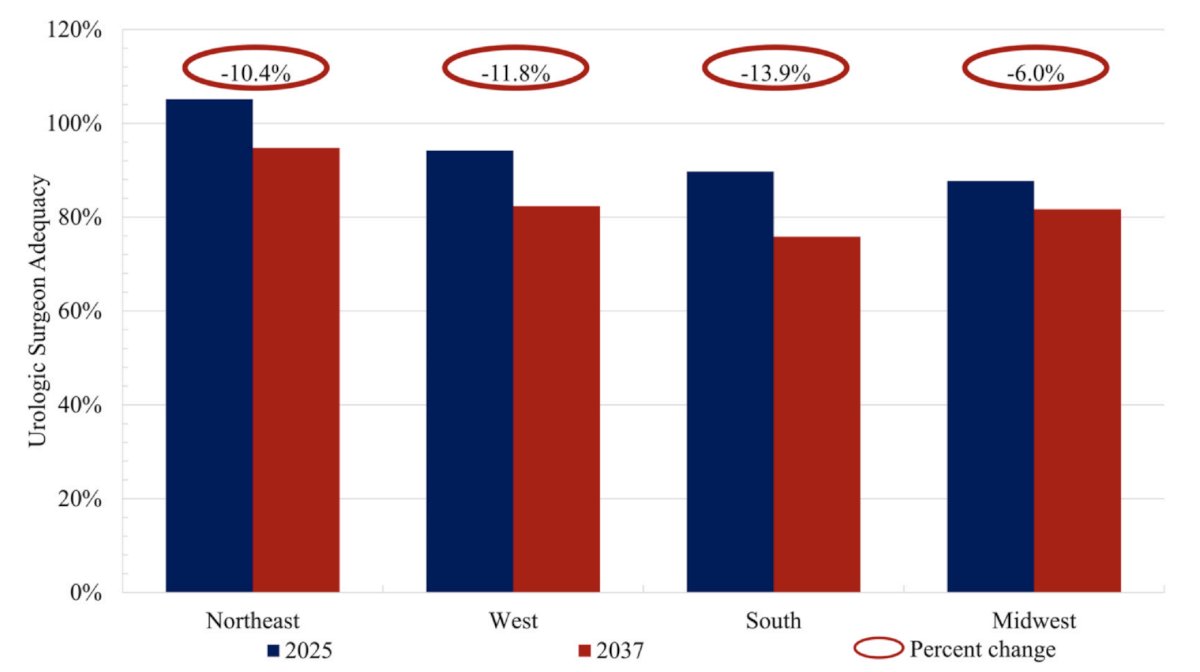

The South and Midwest had the lowest adequacy, and the Northeast had the highest (p < 0.001):

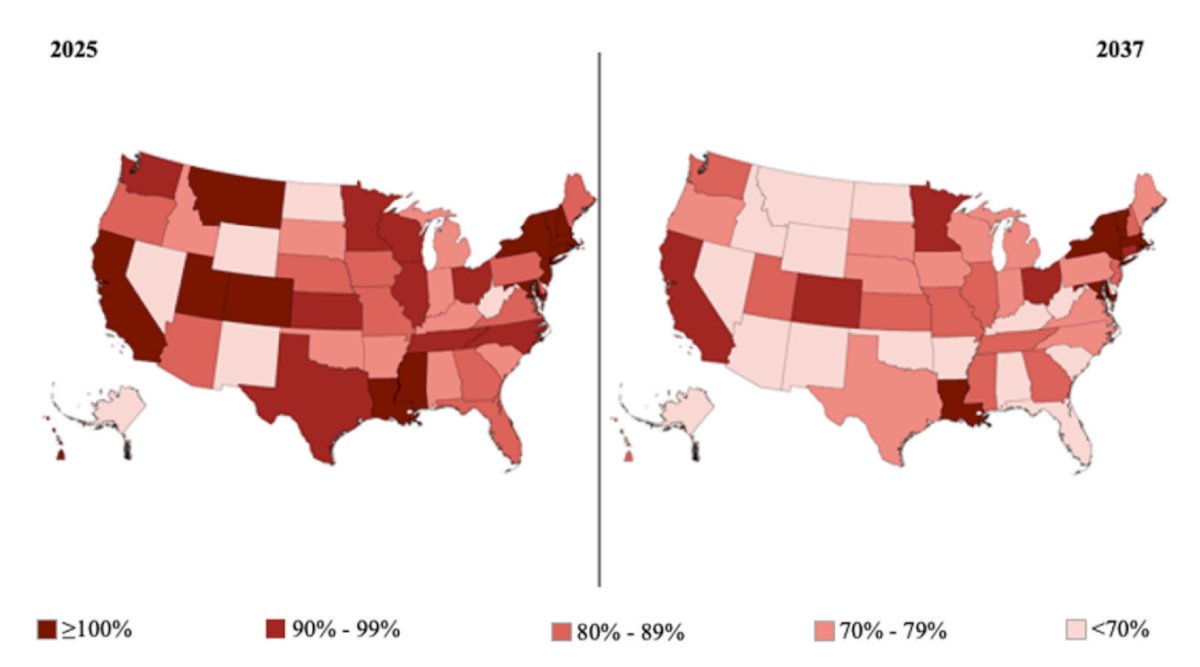

In 2025, the states with the lowest adequacy were Nevada (54.5%), West Virginia (55.6%), and New Mexico (62.5%). By 2037, the states with the lowest projected adequacy were North Dakota (25.0%), Wyoming (33.3%), and Nevada (41.7%):

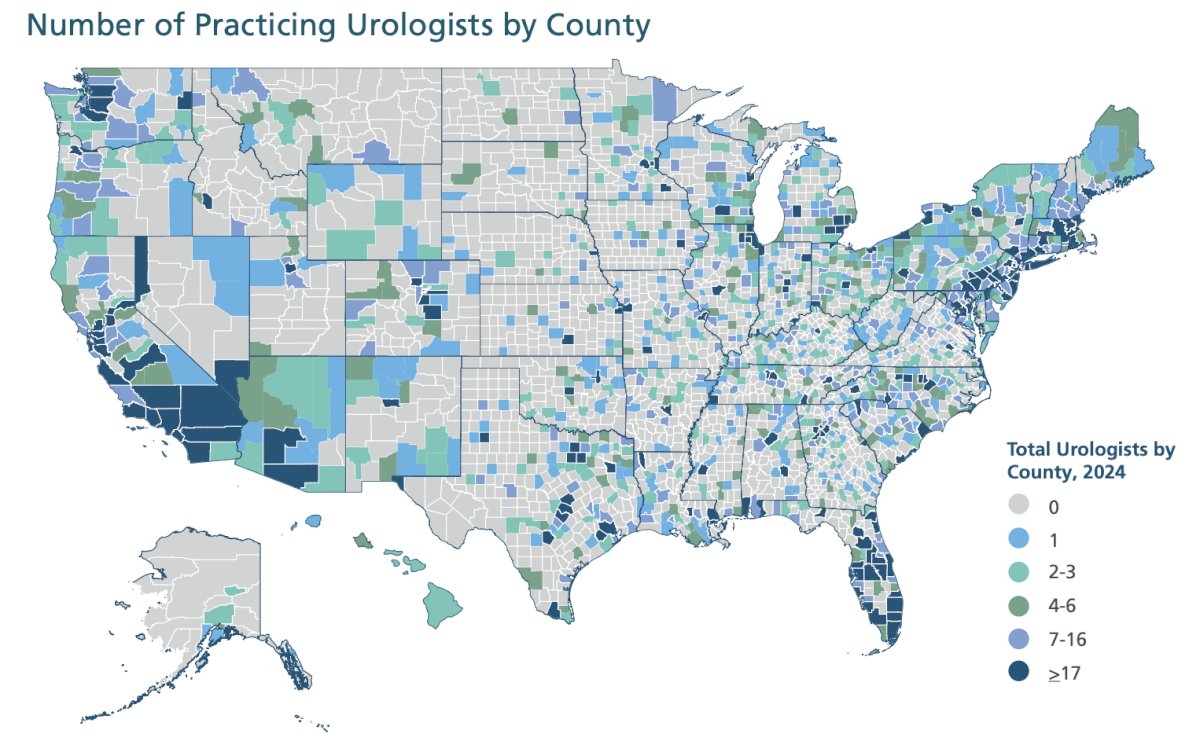

Based on the AUA 2024 census, the following figure shows the number of practicing urologists by county:

Presented at AUA 2025, Baskin et al.3 quantified the extent of urologic services being provided beyond the reported primary practice settings of urologists. They found that of the 1,428 counties in the United States where CMS reports urologic services, 350 (24%) had locums activity, with no urologist who is listed as their primary practice site as being in that county:

Based on the Houlihan Lokey Winter 2024 Urologic Care Industry Sector Spotlight, the $77 billion urologic service industry is a large medical specialty with a compelling growth trajectory. Indeed, Urology is an attractive market, with $77 billion in addressable market, a ~5% annual growth rate, and >90% non deferrable payments. There are several compelling characteristics for investing, including:

- High addressable spend per physician and high percentage of patient wallet share create outsized growth opportunities that are only accessible with scale

- Significant ancillary opportunities for platforms of scale, including the build-out of ambulatory surgery centers

- Favorable site of care shift dynamics, as payors continue to shift care outside of the hospital

- Aging, increasingly unhealthy population, and increased urologic care utilization among younger adults

- New, less invasive treatments driving utilization and increased spending

- Ability to act as an essential PCP for men, covering a wide variety of treatments, capturing the entire care continuum, and facilitating repeat visits

- Multi-specialty expansion opportunities, particularly into GI, women’s health, and oncology

Urology care covers a wide range of medical conditions, treatment, and care types. The overwhelming majority of spending is tied to urgent conditions that necessitate timely treatment:

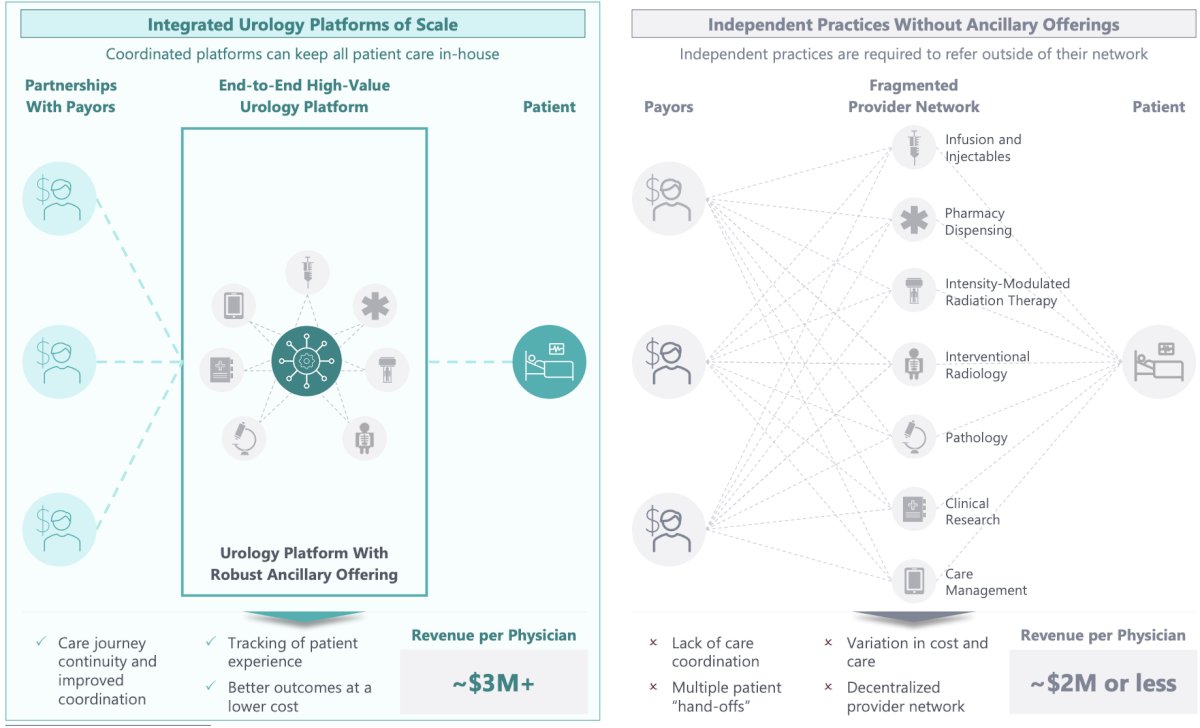

As such, urology is a recession-resilient specialty, with 90%+ of spending attributable to procedures and treatments that cannot be materially avoided or delayed. Finally, Dr. Harris noted that integrated urology practices ‘own’ the patient journey. Integrated, scaled urology platforms drive seamless patient experiences and positive clinical outcomes by “owning” the care journey. Value is added to payors, referral sources, patients, and providers:

Dr. Harris concluded his presentation discussing the state of the Urology workforce with the following take-home points:

- What drives locums tenens and the workforce in Urology is:

- Supply

- Demand

- Controlled distribution

- Economic opportunity

Presented by: Andrew Harris, MD, University of Kentucky, Lexington, KY

Written by: Zachary Klaassen, MD, MSc – Urologic Oncologist, Associate Professor of Urology, Georgia Cancer Center, Wellstar MCG Health, @zklaassen_md on Twitter during the 2026 Southeastern Section of the American Urological Association (SESAUA) Annual Meeting, San Juan, PR, Wed, Mar 18 – Sat, Mar 21, 2026.

References:

- Nam CS, Daignault-Newton S, Kraft KH, et al. Projected US Urology Workforce per Capita, 2020-2060. JAMA Netw Open. 2021 Nov 1;4(11):e.2133864.

- Silvestre J, Seeger S, Reitman CA, et al. Assessing the supply, demand, and adequacy of urologic surgeons in the United States: Forecasting Shortages to 2037. Urology. 2025 Dec:206:235-241.

- Baskin AS, Bowman M, Barocas DA, et al. IP04-35 Quantifying Locums Urology: A quarter of counties with urologic services lack a urologist. J Urol. 2025; May 1;213(5S):e226.