(UroToday.com) The 2026 SESAUA annual meeting featured a health services research session and presentation by Ryan Wong discussing mortality and disability adjusted life years in relation to United States tobacco taxation.

The causal link between smoking and bladder cancer development is well-established, but the long-term impact of tobacco taxation on bladder cancer mortality and disability adjusted life years has not been fully elucidated. Given the protracted latency of carcinogenesis, this study examined whether historical changes in tobacco taxation are associated with reductions in bladder disease burden and mortality in the United States.1

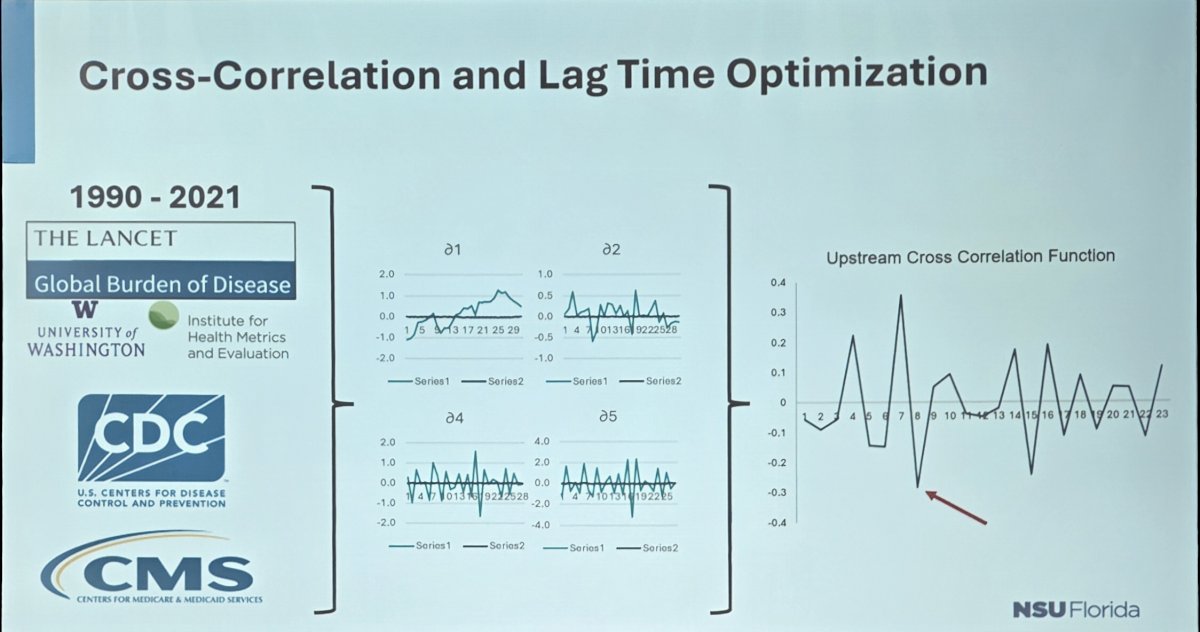

Smoking-attributable bladder cancer mortality and disability adjusted life year data, and federal and state tobacco taxation data were differenced as time series to achieve stationarity. Cross-correlation analysis identified optimal lag times. A semi-logarithmic multivariable linear regression was used to estimate the percent change in bladder cancer outcomes per 1% increase in tobacco tax. Analyses were adjusted for national health expenditures and stratified by state:

The median lag time between tobacco tax changes and smoking-attributable bladder cancer mortality was 17 years, whereas the lag to disability adjusted life years was 24 years:

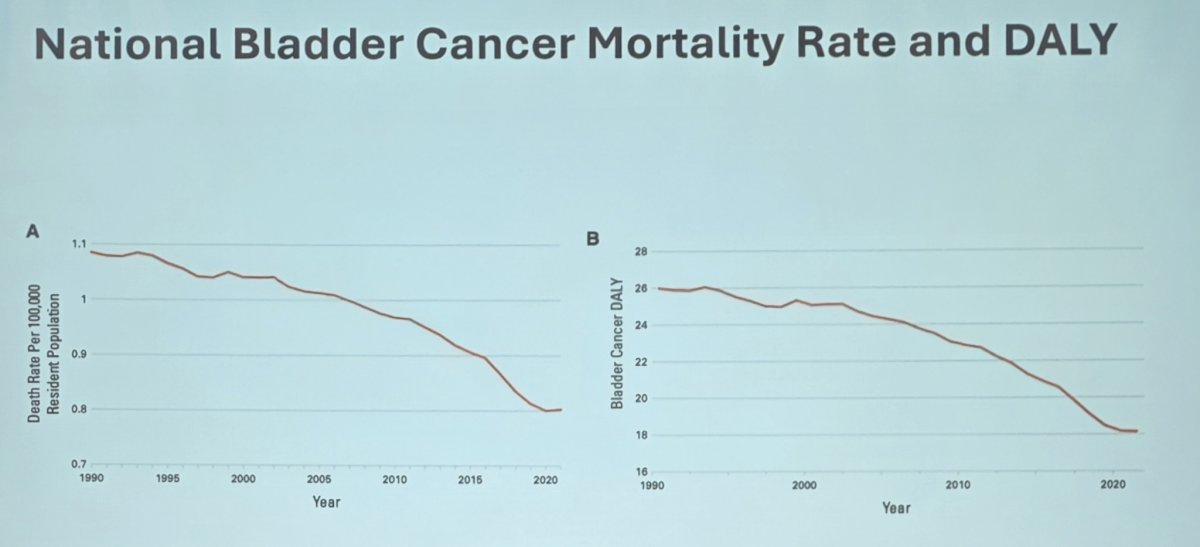

National-level regression showed no significant association between taxation and bladder cancer mortality (-0.09%, p = 0.64) or disability adjusted life years (1.77%, p = 0.051). However, 22 states exhibited significant reductions in mortality, with the greatest observed in Arkansas (-3.64%, P < .001), California, and Indiana. Sixteen states showed significant disability adjusted life years reductions, led by California (-4.68%):

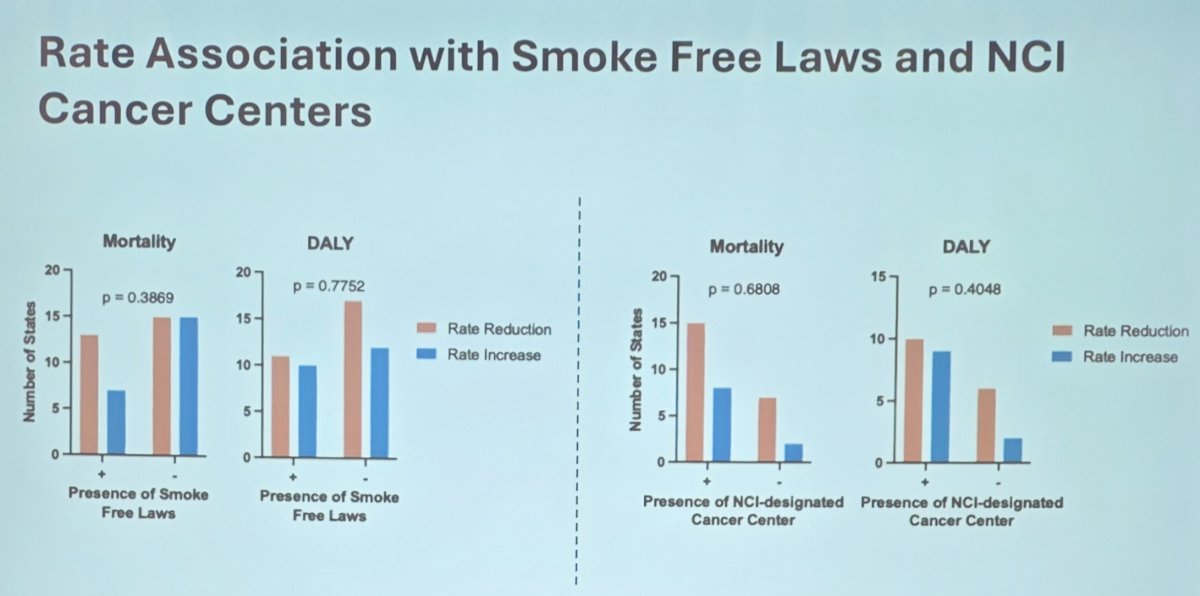

The implementation of smoke-free laws alone was not associated with decreases in smoking-attributable bladder cancer mortality and disability adjusted life years:

Ryan Wong concluded his presentation discussing mortality and disability-adjusted life years in relation to United States tobacco taxation with the following take-home points:

- Bladder cancer mortality and disability adjusted life year rates are variable when associated with rising tobacco taxation

- Tobacco tax policy and smoke-free laws are necessary but not sufficient to reduce smoking-attributable bladder cancer mortality and disability adjusted life years

- Associations between states with heightened tobacco taxation and lower bladder cancer mortality and disability adjusted life years are variable

- Advances in bladder cancer management may partially explain some of the observed regional variation, particularly in states where tobacco control policies alone do not fully account for mortality trends

- This heterogeneity suggests tailoring tobacco control approaches to local contexts and ensuring sustained and financial commitment to reduce the long-term burden of tobacco-related disease

- To minimize bladder cancer burden in the United States, a comprehensive control strategy, including consistent implementation of smoke-free laws and supportive smoking cessation programs, should be leveraged

Presented by: Ryan Wong, Nova Southeastern University, Davie, Florida

Written by: Zachary Klaassen, MD, MSc – Urologic Oncologist, Associate Professor of Urology, Georgia Cancer Center, Wellstar MCG Health, @zklaassen_md on Twitter during the 2026 Southeastern Section of the American Urological Association (SESAUA) Annual Meeting, San Juan, PR, Wed, Mar 18 – Sat, Mar 21, 2026.

Reference: